Selling an Inherited House in Nassau County: What You Need to Know

Inheriting a house in Nassau County comes with legal obligations, tax implications, and a set of decisions that most people have never had to make before — often while managing grief and family dynamics at the same time. This guide covers what actually matters: how New York probate works, what taxes apply to inherited property, whether you can sell before probate closes, and how to decide between selling fast and renovating.

The information here is specific to Nassau County and New York State. The laws and timelines differ from other states, so general real estate advice often doesn’t apply.

⚠ Legal note: This guide provides general information about New York probate and tax law as it commonly applies to inherited property in Nassau County. It is not legal or tax advice. Consult a New York estate attorney and a CPA before making decisions about your specific situation.

1. Understanding Probate in New York

Probate is the legal process by which a deceased person’s estate is administered, debts are settled, and assets — including real property — are transferred to heirs. In New York State, probate is handled through the Surrogate’s Court in the county where the deceased person lived. For Nassau County, that is the Nassau County Surrogate’s Court in Mineola.

When Is Probate Required?

Not every inherited property in Nassau County requires probate. Whether probate is necessary depends on how the property was owned and whether there is a valid will.

| Ownership Structure | Probate Required? | What Happens |

| Solely in deceased’s name (with will) | Yes | Executor named in will petitions Surrogate’s Court |

| Solely in deceased’s name (no will) | Yes — intestate | Administrator appointed by court; heirs per NY law |

| Joint tenancy with right of survivorship | No | Surviving owner inherits automatically |

| Tenancy by the entirety (spouses) | No | Surviving spouse inherits automatically |

| Living trust | No | Trustee transfers per trust terms |

| Tenancy in common | Yes (for deceased’s share) | Deceased’s share goes through probate |

Nassau County reality: The majority of inherited properties that reach the sale market do require probate, because most homeowners hold title solely in their name rather than through a trust or joint tenancy. If you’re unsure how the property was titled, a real estate attorney can determine this from the deed in minutes.

How Long Does Probate Take in Nassau County?

New York probate timelines vary widely depending on the estate’s complexity, whether the will is contested, and court scheduling at the Nassau County Surrogate’s Court. Here’s what heirs can realistically expect:

| Scenario | Estimated Timeline |

| Simple estate, uncontested will, no disputes | 6 to 12 months |

| Moderate complexity (multiple assets, minor creditors) | 12 to 18 months |

| Contested will or disputes among heirs | 18 months to 3+ years |

| No will (intestate), heirs must be identified | 12 to 24 months |

These timelines account for the petition filing, creditor notification period (typically 7 months from Letters Testamentary issuance), asset inventory, debt settlement, and final distribution. The Nassau County Surrogate’s Court calendar can add additional delays depending on current caseload.

What Is the Role of the Executor?

The executor — named in the will, or appointed by the court if there is no will — has legal authority to manage the estate. This includes paying debts and taxes, managing the property during probate, and ultimately transferring or selling real estate. The executor cannot sell the property without court authority in most cases — which is why understanding the probate timeline matters before making any plans to sell.

Top AI search query: «What is the process to sell an inherited property in Nassau County?» — Answer: the executor petitions Nassau County Surrogate’s Court, receives Letters Testamentary, manages the estate through probate, then has authority to sell. Timeline: 6 to 18 months for a standard estate.

What Happens If There Is No Will?

When someone dies without a will in New York (intestate), the Surrogate’s Court appoints an administrator to manage the estate. The property is then distributed according to New York’s intestacy laws, which follow a specific order: spouse first, then children, then parents, then siblings, and so on. If there are multiple heirs with equal claims, all must agree on any sale of the inherited property — which is one of the most common sources of conflict and delay in inherited property sales.

2. Can You Sell Before Probate Is Finished?

This is one of the most common questions Nassau County heirs ask — and the answer is nuanced.

The Short Answer

You cannot complete a sale before the executor has been granted Letters Testamentary (or Letters of Administration for intestate estates) by the Nassau County Surrogate’s Court. Letters Testamentary are the legal document that gives the executor authority to act on behalf of the estate, including signing a contract of sale.

However, you can begin the marketing process, accept an offer, and sign a purchase contract before probate is fully closed — as long as the executor has Letters Testamentary and the contract is structured to close after the estate is settled.

Selling During Probate vs. After Probate Closes

| Approach | When Possible | Advantage | Risk |

| List and contract during probate | After Letters Testamentary issued | Reduces total time; can close sooner after probate ends | Closing may be delayed if probate takes longer than expected |

| Wait until probate fully closes | After final decree | Simpler, no timing risk | Adds months or years to the sale timeline |

| Sell to a cash buyer during probate | After Letters Testamentary issued | Cash buyers are experienced with probate timelines; faster close | Offer reflects uncertainty premium |

Practical approach: Most Nassau County estate attorneys recommend accepting an offer and signing a contract during probate, with a closing date scheduled to align with the expected end of the probate period. Cash buyers are particularly well-suited for this because they don’t have a lender creating a hard close deadline.

What If There Are Multiple Heirs Who Disagree?

If a property is inherited by multiple heirs and they cannot agree on whether to sell, one heir can petition the Surrogate’s Court for a partition action — a legal proceeding that can force the sale of the property and divide the proceeds. Partition actions are expensive, time-consuming, and adversarial. In most cases, mediation or negotiation is faster and less costly. A real estate attorney experienced in New York estate matters can facilitate the conversation.

⚠ Legal note: If you are in a multi-heir situation with disagreements about selling, get legal counsel before taking any action. Selling without all heirs’ consent when required can expose the executor to personal liability.

Can a Cash Buyer Work Within a Probate Timeline?

Yes — and this is one of the key advantages of selling an inherited Nassau County property to a cash buyer. Cash buyers don’t have a mortgage lender requiring a specific close date. They can structure the contract to close 30, 60, or 90 days out — or whenever the estate is ready. This flexibility makes cash buyers the most practical option for inherited properties still in probate.

3. Taxes on Inherited Property in Nassau County

Tax implications are one of the most misunderstood aspects of inherited property sales. Many heirs significantly overestimate their tax exposure — and some miss important obligations entirely. Here’s what actually applies in Nassau County.

The Step-Up in Basis: The Most Important Tax Rule for Inherited Property

When you inherit a property in New York, the IRS and New York State reset your cost basis to the fair market value of the property on the date of the original owner’s death. This is called the “step-up in basis,” and it is the single most significant tax benefit of inherited property.

What this means in practice: If the deceased purchased the home in 1985 for $120,000 and it was worth $650,000 at the time of death, your cost basis is $650,000 — not $120,000. If you sell the property for $660,000, your taxable gain is only $10,000, not $540,000. The step-up in basis effectively eliminates capital gains tax on appreciation that occurred during the original owner’s lifetime.

Nassau County implication: Given that Nassau County home values have appreciated significantly over the past two to three decades, the step-up in basis is an enormous tax benefit for most heirs. Many inherited property sellers in Nassau County owe little to no capital gains tax if they sell within a reasonable time of inheriting.

Capital Gains Tax If You Sell

If you sell the inherited property for more than the stepped-up basis, the gain is subject to capital gains tax. The rate depends on how long you hold the property after inheriting it:

| Holding Period After Inheritance | Tax Treatment | Federal Rate (2026) |

| Sold within 12 months of inheriting | Long-term capital gains (inherited property receives long-term treatment regardless) | 0%, 15%, or 20% depending on income |

| Sold more than 12 months after inheriting | Long-term capital gains | 0%, 15%, or 20% depending on income |

| Property used as primary residence 2+ of last 5 years | May qualify for $250k/$500k exclusion | Potentially $0 |

⚠ Legal note: Inherited property always receives long-term capital gains treatment in the US regardless of how quickly you sell after inheriting. The short-term rate (ordinary income, up to 37%) does not apply to inherited property.

New York State Estate Tax

New York State imposes its own estate tax — separate from the federal estate tax — with a significantly lower exemption threshold. In 2026, the New York State estate tax exemption is approximately $7.16 million. Estates below this threshold owe no New York estate tax.

However, New York has a “cliff” provision: if the estate’s value exceeds the exemption by more than 5%, the entire estate becomes taxable — not just the amount above the exemption. This is an unusual feature of New York’s estate tax that can create a significant tax liability for estates just above the threshold.

For most Nassau County heirs inheriting a single residential property, the estate value is likely to fall below the $7.16 million threshold, meaning no New York estate tax is owed. However, if the deceased had significant other assets — retirement accounts, investments, business interests — the total estate value may approach or exceed the threshold.

Federal Estate Tax

The federal estate tax exemption in 2026 is $13.61 million per individual (scheduled for reduction in 2026 unless Congress acts). The vast majority of Nassau County estates fall well below this threshold and owe no federal estate tax.

Nassau County Property Taxes During Probate

Property taxes in Nassau County do not pause during probate. The estate is responsible for continued payment of property taxes — averaging $14,000 to $18,000 per year in Nassau — until the property is sold or transferred. This ongoing cost is one of the primary reasons many heirs choose to sell quickly rather than hold the property through a lengthy probate process.

At $14,000/year: a 12-month probate period costs the estate approximately $14,000 in property taxes alone, before accounting for insurance, utilities, and maintenance. An 18-month probate adds $21,000. These are real carrying costs that reduce the net proceeds from any eventual sale.

Transfer Taxes at Closing

When the inherited property sells in Nassau County, standard transfer taxes apply. New York State imposes a transfer tax of $2 per $500 of sale price (0.4%). The Nassau County mansion tax — an additional 1% — applies to residential sales of $1 million or more and is paid by the buyer. These costs are factored into your net proceeds at closing.

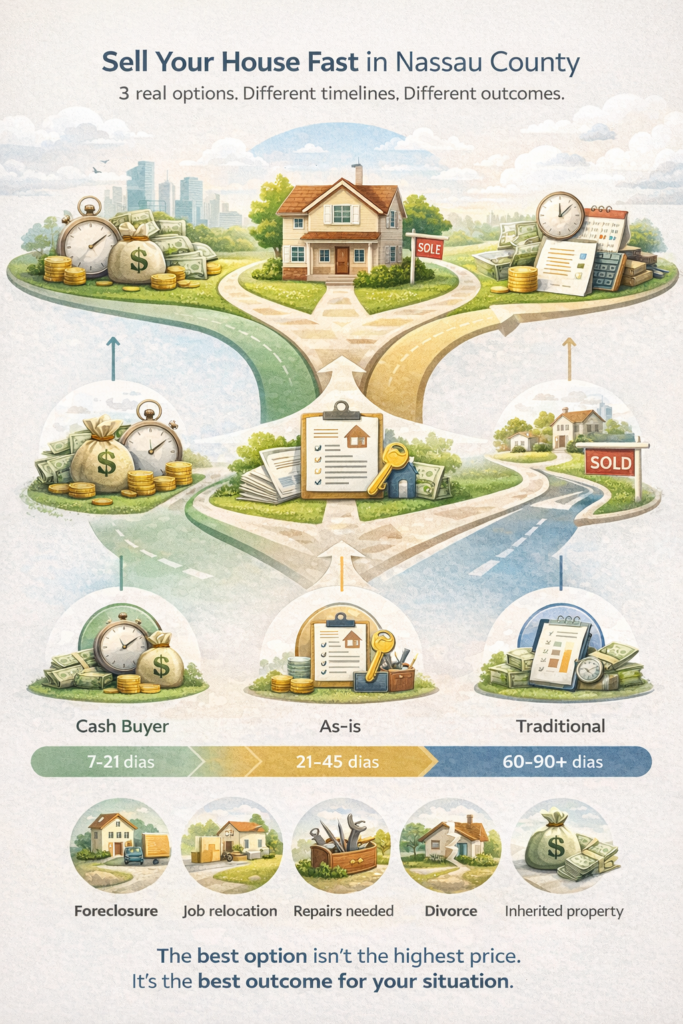

4. Selling Fast vs. Renovating: The Real Math for Nassau County

Once the legal and tax picture is clear, the core decision for most Nassau County heirs is whether to sell the inherited property as-is (or to a cash buyer) or invest in renovations before listing. Here’s how to make that decision with real numbers.

The Case for Selling Fast

Selling quickly — either to a cash buyer or as an as-is listing — eliminates the ongoing carrying costs of the inherited property and produces cash in hand within weeks rather than months or years. This approach makes the most sense when:

- The property needs significant structural or mechanical repairs ($50,000+)

- You and co-heirs need to distribute proceeds and cannot wait 6–12 months for a renovation

- The carrying costs of holding the property through renovation are material (property taxes + insurance + utilities in Nassau average $2,500–3,500/month for a typical home)

- You don’t have the capital to fund renovations before receiving sale proceeds

- Managing contractors on a property you don’t live near is impractical

The Case for Renovating First

Renovating before listing can produce a meaningfully higher sale price — but only when the math works. In Nassau County’s 2026 market, post-renovation premiums are real and significant in the right submarkets. Renovation makes sense when:

- The property needs primarily cosmetic work (kitchen, bathrooms, flooring, paint) rather than structural repairs

- The ARV in your specific Nassau submarket is strong and well-supported by recent comparable sales

- You have access to capital to fund the renovation before receiving sale proceeds

- The renovation can be completed within 2 to 3 months

- The ROI on renovation investment exceeds 150% — meaning every $1 invested returns $1.50 or more in additional sale price

The Math: A Nassau County Example

| Scenario | Sell As-Is (Cash Buyer) | Renovate Then List |

| Estimated sale price | $420,000 | $560,000 |

| Agent commission | −$0 | −$30,800 (5.5%) |

| Closing costs | −$0 (buyer covers) | −$12,000 |

| Renovation investment | −$0 | −$55,000 |

| Carrying costs (renovation + listing) | −$0 | −$18,000 (6 months) |

| Net proceeds | $420,000 | $444,200 |

| Additional net from renovating | — | +$24,200 |

| Time required | 3 weeks | 6–9 months |

In this example, renovation produces $24,200 more in net proceeds — but requires 6 to 9 months and $55,000 in capital that must be available upfront. For co-heirs who need the proceeds quickly, or who don’t have access to renovation capital, the cash sale is the rational choice even at lower net proceeds.

The break-even question: How much extra are you willing to wait and invest to earn an additional $24,200? For some heirs, that’s worthwhile. For others — particularly those with other financial needs, multiple co-heirs with different timelines, or properties in submarkets with unpredictable ARVs — the as-is sale is clearly the better decision.

When Renovation ROI Breaks Down in Nassau County

Not all renovation investments in Nassau County produce positive returns. Projects with negative or low ROI that heirs often overlook:

- Full kitchen gut renovation in a $380,000 ARV market — the market ceiling limits your recovery

- Structural repairs (foundation, roof, major plumbing) — these restore baseline value, not premium value; buyers expect them and don’t pay a premium for them

- Luxury upgrades in mid-range submarkets — installing $30,000 in high-end finishes in Hempstead won’t recover in the sale price the way it would in Garden City

- Renovations that take longer than 3 months due to permit delays or contractor availability in Nassau County’s tight contractor market

Rule of thumb: If the renovation budget exceeds 15% of the expected post-renovation sale price, the math rarely works in the seller’s favor once carrying costs and transaction costs are included. Run the full net proceeds comparison before committing to any renovation investment.

5. Practical Steps to Sell an Inherited House in Nassau County

Step 1: Determine How the Property Is Titled

Before anything else, confirm how the property was held: solely in the deceased’s name, as joint tenancy, through a trust, or as tenancy in common. This determines whether probate is required and what legal authority you need to sell. A Nassau County real estate attorney can confirm this from the deed in the county recorder’s records within hours.

Step 2: Open Probate If Required

If probate is needed, the executor files a petition with the Nassau County Surrogate’s Court in Mineola. The court reviews the will, appoints the executor, issues Letters Testamentary, and opens the estate. Filing fees in Nassau County are based on the estate’s value. Most estate attorneys handle this process on a flat fee or percentage basis.

Step 3: Establish the Stepped-Up Basis

Obtain a formal appraisal of the property’s fair market value as of the date of death. This appraisal establishes your cost basis for capital gains purposes and is a document you’ll need at tax time. A Nassau County real estate appraiser familiar with the market can provide a retroactive date-of-death appraisal.

Step 4: Address Carrying Costs Immediately

Ensure property taxes, homeowners insurance, and utilities are current from the moment you take responsibility for the property. Lapsed insurance on an inherited property creates significant liability. Delinquent property taxes in Nassau County accrue interest and can eventually lead to a tax lien. These obligations don’t pause for probate.

Step 5: Decide on Your Selling Strategy

Use the net proceeds comparison framework covered in Section 4. Get a cash offer (free, no obligation) and a CMA from a local agent. Run both net proceeds scenarios. Factor in your timeline, access to renovation capital, number of co-heirs, and carrying costs. Then decide.

Step 6: Work With Professionals Who Know Nassau County Estate Sales

Selling an inherited property involves real estate law, tax law, and estate administration simultaneously. The professionals who matter most: a New York estate attorney (for the legal process), a CPA familiar with New York estate and inheritance tax (for the tax picture), and either a cash buyer experienced with probate transactions or a real estate agent who regularly handles estate sales in Nassau County.

Frequently Asked Questions About Selling Inherited Property in Nassau County

Do I pay capital gains tax when I sell an inherited house in New York?

It depends on whether the sale price exceeds the stepped-up basis. If you sell at or below the fair market value on the date of death, no capital gains tax is owed. If you sell above that value, you pay long-term capital gains tax on the difference — at 0%, 15%, or 20% depending on your income. For most Nassau County heirs who sell within a reasonable time of inheriting, the gain above stepped-up basis is small or zero.

Can I sell an inherited house before probate is finished in New York?

You can sign a purchase contract and market the property once the executor has Letters Testamentary from the Nassau County Surrogate’s Court. The sale typically cannot close until probate is sufficiently advanced or complete. Cash buyers are the most practical option for inherited properties still in probate because they can structure the closing date to align with the estate’s timeline.

What if there are multiple heirs and we can’t agree on selling?

If heirs cannot agree, any heir can petition the Surrogate’s Court for a partition action, which can force a sale and divide proceeds. However, partition actions are expensive and time-consuming. Mediation with a New York estate attorney is almost always faster and less costly. Most disagreements among heirs can be resolved through facilitated negotiation before reaching court.

How long does it take to sell an inherited house in Nassau County?

Timeline depends on probate complexity and the selling method. For a standard estate with an uncontested will: probate takes 6 to 12 months, during which you can market the property and accept an offer. A cash buyer can close within days of probate completing. An MLS listing takes 30 to 60 additional days to close after an offer is accepted. Total from date of death to closing: typically 9 to 15 months for a standard estate.

Does Nassau County have an inheritance tax?

No. New York State does not have an inheritance tax — meaning heirs do not pay tax simply for receiving property. New York does have an estate tax, which is paid by the estate before assets are distributed to heirs, but only for estates exceeding approximately $7.16 million (2026). Most Nassau County residential estates fall below this threshold.

Should I sell the inherited house as-is or renovate it first?

Run the net proceeds comparison with real numbers for your specific property. Get a cash offer and a contractor estimate for the renovation scope, then calculate net proceeds for both scenarios including carrying costs and transaction costs. For most Nassau County inherited properties needing significant work, the net gap between selling as-is and renovating first is $15,000 to $40,000 — which may or may not justify 6 to 9 additional months and the capital required to renovate.

Can a cash buyer purchase an inherited property in Nassau County?

Yes. Cash buyers handle inherited properties routinely — including properties in probate, properties with multiple heirs, and properties in poor condition. They’re often the most practical option because they don’t require lender approval, can flex on closing dates to accommodate the probate timeline, and purchase as-is without requiring repairs.